ILS Market Update

21 Jul 2026 • 00:35 GMT

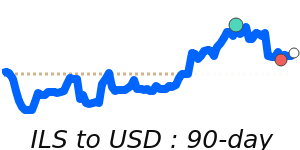

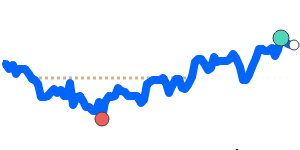

The Israeli shekel has weakened against the US dollar over the past 90 days, trading near 0.3274, which is its lowest point in this period and approximately 3.5% below the average of 0.3393. This decline comes despite a series of positive domestic developments, including the Bank of Israel's surprise rate cut to 4.00% earlier this year, and a 3.5% appreciation against the dollar in the final quarter of 2025. These factors reflect improving economic conditions and regional geopolitical progress, particularly discussions to rebuild regional relations, which have supported the shekel in recent months.

However, recent market movements show volatility, with the shekel experiencing swings up to 9.0%. While regional events and economic data point to continued resilience, the current near-term trend indicates some volatility and downward pressure. Upward movements are possible if regional tensions ease further, but traders should remain mindful of ongoing geopolitical uncertainties and domestic economic factors influencing the shekel's direction.