SEK Market Update

18 Jul 2026 • 01:12 GMT

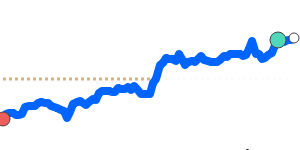

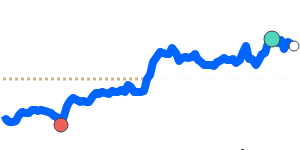

The Swedish krona (SEK) remains relatively steady against major currencies, with recent trade at around 0.1037 USD, slightly below its three-month average. The SEK has traded within a narrow range, indicating stability amidst broader currency movements.

In recent sessions, the US dollar has been supported by rising energy prices, especially due to geopolitical tensions and higher oil costs from the Gulf region. This has kept USD broadly resilient, but the SEK has not wavered much, reflecting some underpinning from Sweden's economic outlook and cautious currency sentiment.

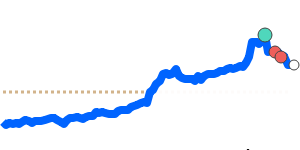

Looking ahead, the SEK could see some support if the US dollar softens, especially if recent dovish signals from the Federal Reserve persist. However, markets are also watching for any Riksbank moves that could influence the krone, particularly if concerns about Swedish inflation or currency depreciation grow.

Overall, the SEK remains within its recent stable trading range, but traders should keep an eye on US energy prices and central bank signals, which can add volatility or directionality to the currency in the near term.

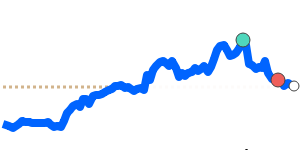

📊 Quick forecast view

🟢 Mild upside

0.1040 – 0.1080

🌍 Global risk sentiment

🟢 Uptrend