Latest market analysis

CAD Market Update

05 Aug 2026 • 00:28 GMT

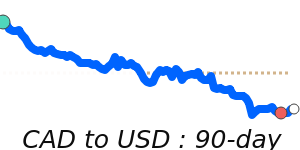

The Canadian dollar remains steady against the US dollar, trading at around 0.711, which is slightly below its three-month average of 0.715. Over recent weeks, the CAD has traded within a narrow range from 0.7026 to 0.7335, reflecting stable market sentiment.

Oil prices continue to influence the CAD’s movements, with recent gains supporting the currency's resilience. Despite expectations for cautious monetary policy from the Bank of Canada, which has kept rates steady at 2.25%, the market is watching for any signs of future hikes. External factors, such as US trade tensions and energy prices, remain important drivers for the CAD.

The outlook for the Canadian dollar is cautiously optimistic. Many analysts forecast the currency could strengthen slightly later in the year, given oil market stability and Canada's economic data. However, fluctuations in energy prices and US greenback strength, impacted by geopolitical events and economic trends, can quickly shift this outlook. For now, the CAD remains within its usual trading range, keeping the door open for potential upside moves if oil prices stay firm and Canadian economic signals remain positive.

Forecast snapshot

Quick CAD/USD forecast

Near-term bias🔴 Mild downside

Expected rangeN/A

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

CAD news & insights

Recent analysis, guides and market developments relevant to the Canadian dollar.

Rate direction

Canadian dollar to US dollar · CAD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on CAD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore CAD pairs

Popular CAD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 CAD =0.7105USD

1D−0.1%▼

1 CAD =0.6159EUR

1D−0.3%▼

1 CAD =12.25MXN

1D−0.6%▼

1 USD =0.8669EUR

1D−0.2%▼

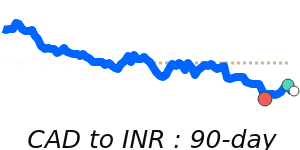

1 CAD =67.56INR

1D−0.4%▼

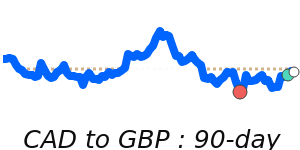

1 CAD =0.5280GBP

1D−0.3%▼

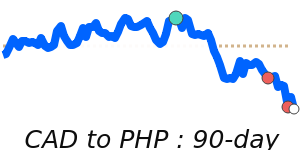

1 CAD =43.17PHP

1D0.0%⬦

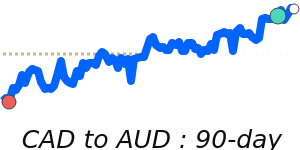

1 CAD =1.0082AUD

1D−0.8%▼

1 INR =0.014802CAD

1D+0.4%▲