Latest market analysis

CHF Market Update

11 Aug 2026 • 00:29 GMT

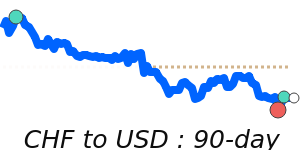

The Swiss franc remains relatively firm against the major currencies, trading about 1.1% below its three-month average against the US dollar at 1.2347. Its recent movements are characterized by stability within a 5% range, with no significant swings. The franc’s strength is supported by ongoing geopolitical uncertainty and the Swiss National Bank’s indication it may intervene if the currency appreciates too rapidly.

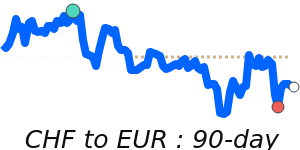

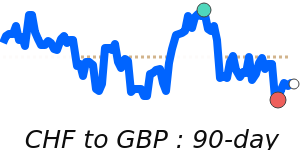

In particular, the CHF is trading near 90-day lows against the British pound at around 0.9136, and close to its three-month average against the euro at approximately 1.0694. These moves highlight that, despite some recent dips, the franc remains resilient as a safe haven amid global tensions.

Traders should monitor potential SNB interventions, which could influence currency movements, especially if the franc continues to press higher. Meanwhile, some pressure persists on Swiss exporters, as a stronger franc makes their goods more expensive abroad. Overall, the Swiss franc is expected to stay supported through 2026, with analysts noting its ongoing appeal for investors seeking safety in uncertain times.

Forecast snapshot

Quick CHF/USD forecast

Near-term bias🟢 Mild upside

Expected range1.2380 – 1.3100

Dominant driver🌍 Global risk sentiment

3-month trend🔴 Downtrend

Stay informed

CHF news & insights

Recent analysis, guides and market developments relevant to the Swiss franc.

Rate direction

Swiss franc to US dollar · CHF/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on CHF exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore CHF pairs

Popular CHF exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 CHF =1.2334USD

1D−0.3%▼

1 CHF =1.0685EUR

1D−0.1%▼

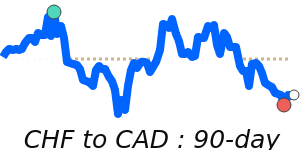

1 CHF =1.7174CAD

1D−0.4%▼

90dLows

1 CHF =0.9131GBP

1D−0.4%▼

90dLows

1 CHF =117.72INR

1D0.0%⬦

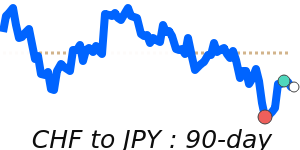

1 CHF =196.46JPY

1D+0.7%▲

1 CHF =1.7465AUD

1D−0.1%▼

1 CHF =1.5787SGD

1D−0.1%▼

1 CHF =8.3201CNY

1D−0.2%▼