Latest market analysis

JPY Market Update

31 Jul 2026 • 00:27 GMT

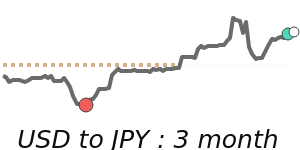

The Japanese yen has recently traded around 163 against the dollar, reaching levels not seen since 1986. The move reflects ongoing pressure from higher interest rate differentials and rising oil prices, which support the dollar and the carry trade. While the Bank of Japan has yet to make any major changes, some traders wondered if a rate hike might come sooner, but no action has been taken.

The yen's decline has been driven mainly by external factors such as geopolitical tensions and higher energy costs, which bolster the US dollar. Despite some speculation that Japanese authorities might intervene to boost the yen, no significant shifts have occurred yet. Market participants continue to monitor postures from Japan’s financial officials and U.S. interest rate trends, which could influence the yen’s future direction.

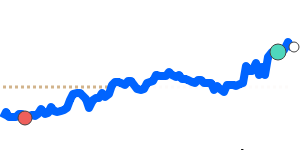

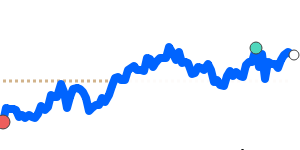

Overall, the USD/JPY pair remains within a range close to the 3-month average. Many banks anticipate the yen could weaken further by year-end, with some forecasting a move towards 160 or higher if current trends persist. However, any surprise intervention from Japan could cause sharp reversals, so traders remain watchful of upcoming policy signals and geopolitical developments.

Forecast snapshot

Quick USD/JPY forecast

Near-term bias🔴 Mild downside

Expected range160.2000 – 163.9000

Dominant driver🌍 Global risk sentiment

3-month trend🔴 Downtrend

Stay informed

JPY news & insights

Recent analysis, guides and market developments relevant to the Japanese yen.

Rate direction

US dollar to Japanese yen · USD/JPY trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on JPY exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore JPY pairs

Popular JPY exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 JPY =0.006328USD

1D+2.0%▲

1 USD =158.04JPY

1D−2.0%▼

1 JPY =0.008869CAD

1D+1.8%▲

1 JPY =0.005484EUR

1D+1.5%▲

1 JPY =0.004692GBP

1D+1.3%▲

1 AED =43.03JPY

1D−2.0%▼

1 JPY =114.09IDR

1D+1.9%▲

1 MYR =38.69JPY

1D−1.8%▼

1 AUD =111.26JPY

1D−1.1%▼