Latest market analysis

MXN Market Update

07 Aug 2026 • 00:32 GMT

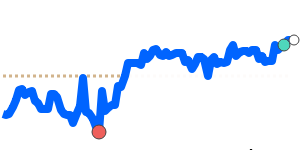

The Mexican peso has recently reached a 60-day high against the US dollar, trading near 0.05812, which is about 1% above its three-month average. This strength comes amid Mexico’s steady interest rates, which continue to support the peso through attractive carry trades. Risk sentiment has also been positive, thanks to better geopolitical news and a calm market outlook.

While the peso remains resilient, traders should watch for upcoming developments. Changes in US Federal Reserve policy or US economic data, especially inflation figures, could impact the dollar and, consequently, the MXN. Additionally, external factors like global risk appetite shifts or negotiations on trade agreements could introduce short-term fluctuations.

Compared to other currencies, the peso has been steady, also reaching recent highs versus the euro and Australian dollar. These moves reflect broader market confidence and Mexico’s stable economic backdrop. Overall, the peso remains well-supported but, as always, remain aware of external risks that could influence its direction in the coming weeks.

Forecast snapshot

Quick MXN/USD forecast

Near-term bias⚪ Range-bound

Expected range0.0570 – 0.0580

Dominant driver⚖️ Interest-rate differentials

3-month trend🔴 Downtrend

Stay informed

MXN news & insights

Recent analysis, guides and market developments relevant to the Mexican peso.

Rate direction

US dollar to Mexican peso · USD/MXN trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on MXN exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore MXN pairs

Popular MXN exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 MXN =0.058356USD

1D+0.2%▲

1 MXN =0.050476EUR

1D+0.4%▲

90dHighs

1 MXN =0.081410CAD

1D+0.2%▲

1 MXN =0.043256GBP

1D+0.3%▲

1 MXN =5.5519INR

1D+0.4%▲

1 MXN =9.2089JPY

1D+0.6%▲

1 MXN =0.082587AUD

1D+0.5%▲

1 MXN =0.074585SGD

1D+0.4%▲

90dHighs

1 MXN =0.3937CNY

1D+0.2%▲