Latest market analysis

MXN Market Update

08 Aug 2026 • 01:29 GMT

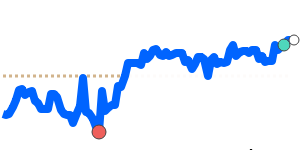

The Mexican peso recently hit 90-day highs against the US dollar, trading near 0.058356, which is about 1.4% above its three-month average. Despite this advance, the peso remains within a stable trading range, with little recent volatility.

The strength of the peso is supported by Banxico's decision to hold interest rates steady, reinforcing its appeal to carry traders. Attractive yields and cautious optimism around Mexico’s economy are also helping the currency stay resilient. However, ongoing geopolitical concerns, including U.S.-Iran relations and global risk appetite, could influence the peso’s direction in the near term.

Against other major currencies, the peso also reached 90-day highs versus the euro and Canadian dollar. Still, movement has been modest, with the peso trading within narrow ranges, reflecting a balanced market.

Overall, the peso’s recent gains are a positive sign, but traders should stay attentive to potential market shifts driven by external geopolitical developments or changes in monetary policy from Banxico or the Fed.

Forecast snapshot

Quick MXN/USD forecast

Near-term bias🔴 Mild downside

Expected range0.0570 – 0.0580

Dominant driver🌍 Global risk sentiment

3-month trend🔴 Downtrend

Stay informed

MXN news & insights

Recent analysis, guides and market developments relevant to the Mexican peso.

Rate direction

US dollar to Mexican peso · USD/MXN trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on MXN exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore MXN pairs

Popular MXN exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 MXN =0.058356USD

1D+0.4%▲

90dHighs

1 MXN =0.050476EUR

1D+0.1%▲

90dHighs

1 MXN =0.081410CAD

1D0.0%⬦

1 MXN =0.043256GBP

1D+0.2%▲

1 MXN =5.5519INR

1D+0.2%▲

1 MXN =9.2089JPY

1D0.0%⬦

1 MXN =0.082587AUD

1D−0.1%▼

1 MXN =0.074585SGD

1D0.0%⬦

90dHighs

1 MXN =0.3937CNY

1D+0.4%▲