PHP Market Update

23 Jul 2026 • 00:34 GMT

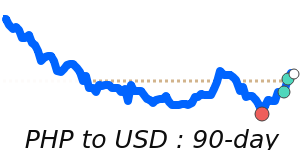

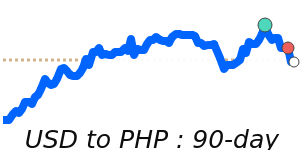

The Philippine peso (PHP) has recently traded near its 30-day lows against the US dollar, at around 0.016185, which is just below its 3-month average of 0.016307. Despite this short-term dip, the currency has been quite stable within a 2.6% range. The broader dollar outlook suggests the USD is expected to retain moderate strength, supported by safe-haven demand amid geopolitical tensions, especially around the Strait of Hormuz, and rising oil prices.

While the PHP has faced downward pressure recently, ideal exports, investments, and external balances remain key. Some forex forecasts indicate the USD/PHP could rise to around 62.7 by year's end, driven by US dollar strength. However, others anticipate the pair to move within the 60.00 to 61.50 range, reflecting potential stabilization.

For retail traders, it's important to monitor US dollar movements, geopolitical risks, and oil prices, as these factors could influence the PHP exchange rate further. Currently, the PHP remains relatively stable but close to recent lows against the USD.

📊 Quick forecast view

🔴 Mild downside

0.0160 – 0.0170

🏦 Central bank policy divergence

🟢 Uptrend