PHP Market Update

24 Jul 2026 • 00:33 GMT

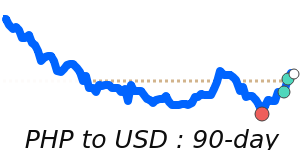

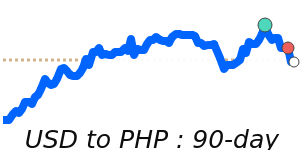

The Philippine peso remains near its 90-day lows against the US dollar, trading at approximately 0.016164, which is just under 1% below its average over the past three months. The currency has been stable within a narrow range of 2.6%, indicating limited recent volatility.

Overall, the US dollar remains relatively strong amid ongoing geopolitical tensions and market caution. The dollar's strength is supported by safe-haven flows, oil prices hovering near USD 100 per barrel, and cautious expectations around US interest rate policies. These factors are keeping the USD's upward pressure on the peso intact.

Looking ahead, if geopolitical tensions escalate or if the Fed hints at longer-term interest rate hikes, the USD could continue to strengthen against the PHP. Conversely, local economic developments or shifts in global risk sentiment might stabilize or even weaken the dollar's influence on the peso.

For traders, it’s important to stay attentive to global geopolitical updates, Fed comments, and oil price movements, all of which could impact the PHP/USD exchange rate in the weeks ahead.

📊 Quick forecast view

🔴 Mild downside

0.0160 – 0.0170

🏦 Central bank policy divergence

🟢 Uptrend