Latest market analysis

AUD Market Update

04 Aug 2026 • 00:28 GMT

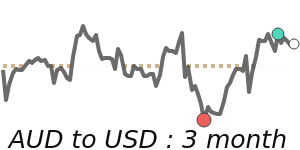

The Australian dollar is trading around 0.7000 against the US dollar, staying close to its three-month average of 0.7047. Recent activity shows the AUD/USD has been stable within a range of roughly 0.6887 to 0.7258 over the past few months, with the current level just 0.7% below the average.

Market sentiment is cautious as traders await key economic data, like Australia's inflation report, and decisions from the Federal Reserve in the US. The Aussie’s recent dip toward 0.6990 reflects this uncertainty. The currency's future direction will likely depend on global developments, including US interest-rate moves and geopolitical factors impacting energy prices.

While the AUD is holding above notable support levels, any further clarity from upcoming economic releases and international policy signals could influence whether it maintains its current range or tests new highs or lows. Overall, the outlook remains balanced, with potential for modest gains if international conditions favor Australian exports and interest rates remain stable.

Forecast snapshot

Quick AUD/USD forecast

Near-term bias🔴 Mild downside

Expected range0.6770 – 0.7000

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

AUD news & insights

Recent analysis, guides and market developments relevant to the Australian dollar.

Rate direction

Australian dollar to US dollar · AUD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on AUD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore AUD pairs

Popular AUD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 AUD =0.7020USD

1D−0.7%▼

1 AUD =0.6100EUR

1D−0.3%▼

1 AUD =110.64JPY

1D−0.5%▼

1 AUD =1.1963NZD

1D−0.1%▼

1 AUD =66.92INR

1D−0.8%▼

1 AUD =12,657IDR

1D−1.1%▼

1 AUD =0.9007SGD

1D−0.6%▼

1 AUD =2.8732MYR

1D−0.4%▼