Latest market analysis

DKK Market Update

11 Aug 2026 • 00:30 GMT

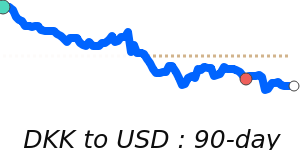

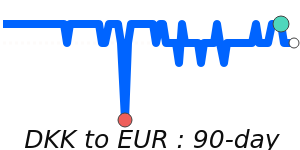

The Danish krone remains relatively stable against the US dollar, trading at around 0.1545, just above its three-month average. Over the past few weeks, the DKK has traded within a narrow 3.4% range, reflecting limited volatility. Despite high levels of EUR/DKK exchange rates approaching historic highs, the Danish central bank has largely maintained a cautious approach, with no significant intervention so far.

US dollar strength continues to be supported by expectations of Federal Reserve rate hikes, driven by strong employment data and rising energy prices. Market participants are closely watching for any shifts in Fed policy signals that could influence USD movements.

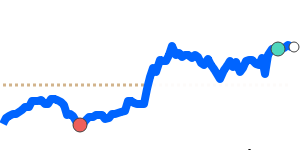

Against other currencies, the DKK is holding steady; for example, it’s near its average against the AUD and JPY, indicating resilience amidst global market fluctuations. The currency’s stable position suggests traders are cautious amid the current geopolitical and economic backdrop, with no clear signs of aggressive intervention from Denmark’s authorities in the near term. This environment points toward a measured approach as the market watches for developments that may impact the DKK's direction.

Forecast snapshot

Quick DKK/USD forecast

Near-term bias🔴 Mild downside

Expected range0.1550 – 0.1580

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

DKK news & insights

Recent analysis, guides and market developments relevant to the Danish krone.

Rate direction

US dollar to Danish krone · USD/DKK trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on DKK exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore DKK pairs

Popular DKK exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 DKK =0.1543USD

1D−0.1%▼

1 DKK =0.1338EUR

1D0.0%⬦

1 DKK =0.2150CAD

1D−0.3%▼

1 DKK =0.1143GBP

1D−0.3%▼

1 DKK =14.72INR

1D+0.1%▲

1 DKK =24.58JPY

1D+0.7%▲

1 DKK =0.2186AUD

1D0.0%⬦

1 DKK =0.1977SGD

1D+0.1%▲

1 DKK =1.0412CNY

1D−0.1%▼