Latest market analysis

EUR Market Update

06 Aug 2026 • 00:28 GMT

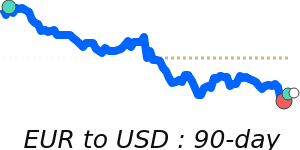

The euro has recently strengthened against the US dollar, hitting 30-day highs near 1.1557. This move comes after a period of relative stability, with EUR/USD trading within a narrow 3.8% range from 1.1359 to 1.1789 over the past three months. The current level is slightly above the 3-month average, indicating a modest rally.

Market attention remains focused on US monetary policy amid ongoing geopolitical tensions and energy price fluctuations. Despite US inflation data showing some softening last week, traders are weighing the possibility of an additional rate hike by the Federal Reserve, which could influence dollar strength in the coming months. Meanwhile, the euro faces headwinds from a cautious tone around Eurozone economic indicators and upcoming ECB policy decisions.

While some bank forecasts see the EUR/USD ending the year around 1.15 with a stronger dollar, others expect a modest increase toward 1.18 if US rates pause or soften. Overall, the euro is holding steady amid these conflicting signals, with its near-term trajectory likely to be influenced by Fed policy outlooks and eurozone economic updates.

Forecast snapshot

Quick EUR/USD forecast

Near-term bias🔴 Mild downside

Expected range1.1560 – 1.1790

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

EUR news & insights

Recent analysis, guides and market developments relevant to the euro.

Rate direction

Euro to US dollar · EUR/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on EUR exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore EUR pairs

Popular EUR exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 EUR =1.1543USD

1D+0.2%▲

1 EUR =1.6172CAD

1D−0.2%▼

1 EUR =0.8574GBP

1D+0.1%▲

1 EUR =4.7216MYR

1D+0.2%▲

1 EUR =1.6397AUD

1D+0.1%▲

1 EUR =4.2391AED

1D+0.2%▲

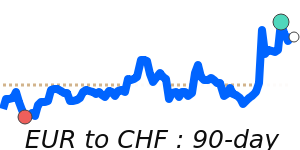

1 EUR =0.9334CHF

1D−0.1%▼

90dHighs

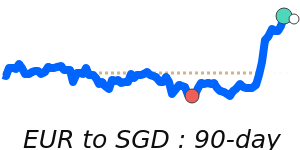

1 EUR =1.4800SGD

1D+0.1%▲