Latest market analysis

HKD Market Update

08 Aug 2026 • 01:26 GMT

The HKD remains near its 90-day lows against the USD, trading around 0.1275, close to its three-month average. Despite this slight dip, the currency has held within a narrow 0.2% range from 0.1275 to 0.1277, reflecting stability under the current peg system with the USD. This stability is supported by Hong Kong's recent economic outlook, including a fiscal surplus and firm monetary policy alignment with the U.S. Federal Reserve, which maintained its rate at 4% in January.

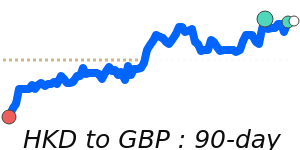

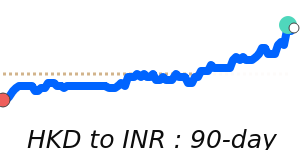

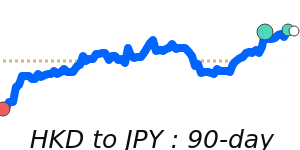

Meanwhile, the HKD has also seen minimal movement against other major currencies. It trades near recent lows against the EUR and GBP, with the HKD/EUR around 0.1103 and HKD/GBP close to 0.094475, both in line with their recent ranges. Against the JPY, the HKD is at about 20.12, slightly below its three-month average, indicating limited volatility.

Overall, the HKD's performance continues to reflect the stability of Hong Kong’s macro outlook and its strong linkage to the USD. As long as US interest rates remain steady and geopolitical developments stay contained, the HKD is expected to stay within its current trading range through the coming months.

Stay informed

HKD news & insights

Recent analysis, guides and market developments relevant to the Hong Kong dollar.

Rate direction

US dollar to Hong Kong dollar · USD/HKD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on HKD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore HKD pairs

Popular HKD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 HKD =0.1275USD

1D0.0%⬦

90dLows

1 HKD =0.1103EUR

1D−0.3%▼

1 HKD =0.1779CAD

1D−0.4%▼

1 HKD =0.094453GBP

1D−0.3%▼

1 HKD =12.13INR

1D−0.2%▼

1 HKD =20.11JPY

1D−0.4%▼

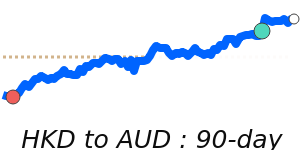

1 HKD =0.1805AUD

1D−0.5%▼

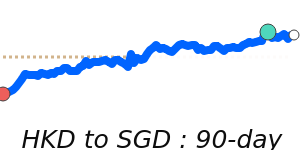

1 HKD =0.1629SGD

1D−0.4%▼

1 HKD =0.8600CNY

1D0.0%⬦

90dLows