Latest market analysis

NZD Market Update

04 Aug 2026 • 00:29 GMT

The New Zealand dollar remains relatively stable against the US dollar, trading at around 0.5866 — just slightly above its three-month average of 0.5818. The pair has mostly stayed within a narrow range, moving between 0.5640 and 0.5988. Recent strength in NZD has been supported by the Reserve Bank of New Zealand's recent rate hike and signs of improving economic data, such as strong manufacturing figures.

However, US dollar movements could influence the NZD in the coming months, especially if US Federal Reserve policy shifts or economic data surprise markets. For now, the NZD continues its modest gains against the euro, at about 0.5098, and against the British pound at 0.4369 — both close to their recent averages.

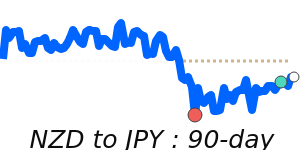

Against the Japanese yen, the NZD remains near 92.41, a little below its three-month average, indicating limited volatility there. Overall, the NZD remains well within its recent trading range, with upcoming economic updates and central bank guidance likely to be key factors shaping its direction.

Forecast snapshot

Quick NZD/USD forecast

Near-term bias🔴 Mild downside

Expected range0.5730 – 0.5870

Dominant driver🌍 Global risk sentiment

3-month trend🟢 Uptrend

Stay informed

NZD news & insights

Recent analysis, guides and market developments relevant to the New Zealand dollar.

Rate direction

New Zealand dollar to US dollar · NZD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on NZD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore NZD pairs

Popular NZD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 NZD =0.5866USD

1D−0.6%▼

1 NZD =0.8357AUD

1D+0.1%▲

90dHighs

1 NZD =0.4369GBP

1D−0.1%▼

1 NZD =92.43JPY

1D−0.3%▼

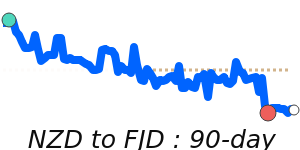

1 NZD =1.2998FJD

1D−0.7%▼

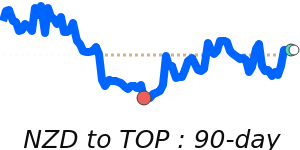

1 NZD =1.4123TOP

1D−0.6%▼

1 NZD =2.4004MYR

1D−0.3%▼

90dHighs

1 NZD =1.6168WST

1D−0.6%▼