Latest market analysis

NZD Market Update

08 Aug 2026 • 01:26 GMT

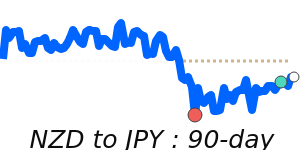

The New Zealand Dollar (NZD) remains relatively strong against the US dollar, trading at around 0.5894. This is about 1.3% above its three-month average of 0.5816. The NZD has seen limited swings recently, staying within a stable range, and is near seven-day highs against the Japanese yen at roughly 93.01, just below its recent three-month average.

The kiwi's recent strength is supported by the Reserve Bank of New Zealand’s (RBNZ) decision to hike rates by 25 basis points, aligning with market expectations. Economic data in New Zealand, like strong manufacturing figures, also bolster confidence in the currency. However, global factors, particularly concerns over Chinese demand and geopolitical tensions, continue to influence the outlook.

While the NZD is slightly above its longer-term averages, analysts forecast some stabilization ahead. The currency could face pressure from U.S. Federal Reserve policy moves or changes in global risk sentiment. Nonetheless, with the potential for ongoing RBNZ support, the NZD may hold its position near current levels into the near future.

Forecast snapshot

Quick NZD/USD forecast

Near-term bias🔴 Mild downside

Expected range0.5880 – 0.5990

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

NZD news & insights

Recent analysis, guides and market developments relevant to the New Zealand dollar.

Rate direction

New Zealand dollar to US dollar · NZD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on NZD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore NZD pairs

Popular NZD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 NZD =0.5878USD

1D+0.4%▲

1 NZD =0.8332AUD

1D−0.1%▼

1 NZD =0.4365GBP

1D+0.2%▲

1 NZD =92.77JPY

1D0.0%⬦

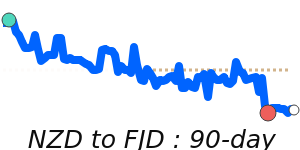

1 NZD =1.2983FJD

1D+0.1%▲

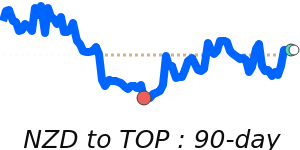

1 NZD =1.4154TOP

1D+0.4%▲

1 NZD =2.4044MYR

1D+0.4%▲

1 NZD =1.6203WST

1D+0.4%▲