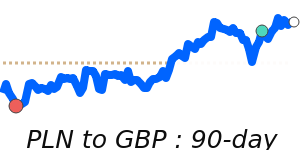

PLN Market Update

23 Jul 2026 • 00:30 GMT

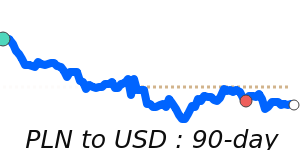

The Polish zloty (PLN) has seen some modest moves against major currencies recently. It trades at around 0.2637 against the US dollar, about 2.7% below its 3-month average of 0.2709. The USD's recent strength is supported by safe-haven demand amid geopolitical tensions, especially around the Strait of Hormuz and rising oil prices. This upward pressure on the dollar has kept the PLN/USD rate below its recent average, although fluctuations have been limited within a 6% range.

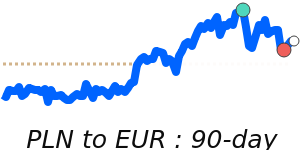

Against the euro, the PLN is at roughly 0.2310, about 1.5% below its 3-month average, with the currency pair holding steady within a narrow range. The momentum for the zloty remains supported by Poland's positive economic outlook and modest monetary easing, which keeps the PLN relatively resilient.

Over the longer term, forecasts from UBS suggest the EUR/PLN will hover around 4.20 in the first quarter of 2026, reflecting Poland’s solid growth prospects. Overall, while the USD has edged higher due to safe-haven flows, the PLN remains within the range influenced by local fundamentals and global risk sentiment.

📊 Quick forecast view

🔴 Mild downside

0.2580 – 0.2640

🌍 Global risk sentiment

⚪ Range-bound