Latest market analysis

PLN Market Update

05 Aug 2026 • 00:31 GMT

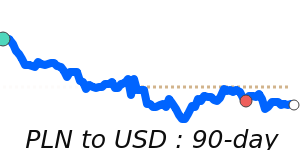

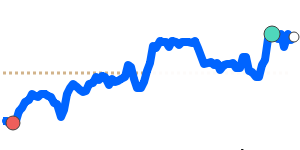

The Polish zloty (PLN) remains near its recent 30-day high against the US dollar, trading close to 0.2684. This marks the strongest level in about a month, supported by Poland's stable economic outlook and an easing monetary policy. The NBP’s rate cut to 4% in 2025 and a projected GDP growth of 3.5% in 2026 bolster confidence in the zloty’s resilience.

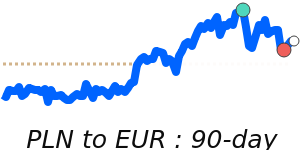

Meanwhile, the EUR/PLN has also edged higher, nearing 0.2328, reflecting Poland’s solid growth prospects and a carry advantage over the euro. The currency’s stability is further evidenced by limited volatility in recent weeks.

Although the zloty has strengthened against the dollar and euro, it remains within normal trading ranges, indicating cautious optimism among investors. External factors, such as US energy prices and geopolitical tensions, continue to influence USD strength, while Poland’s favorable economic fundamentals support the zloty’s current position. Overall, PLN remains well-supported amid a backdrop of steady growth and attractive carry opportunities.

Forecast snapshot

Quick PLN/USD forecast

Near-term bias🔴 Mild downside

Expected range0.2680 – 0.2790

Dominant driver🏦 Central bank policy divergence

3-month trend🟢 Uptrend

Stay informed

PLN news & insights

Recent analysis, guides and market developments relevant to the Polish zloty.

Rate direction

US dollar to Polish zloty · USD/PLN trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on PLN exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore PLN pairs

Popular PLN exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 PLN =0.2680USD

1D+0.6%▲

1 PLN =0.2322EUR

1D+0.3%▲

1 PLN =0.3768CAD

1D+0.7%▲

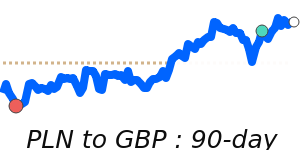

1 PLN =0.1989GBP

1D+0.5%▲

1 PLN =25.49INR

1D+0.3%▲

1 PLN =42.25JPY

1D+1.0%▲

1 PLN =0.3804AUD

1D−0.1%▼

1 PLN =0.3436SGD

1D+0.6%▲

1 PLN =1.8091CNY

1D+0.6%▲