Latest market analysis

SGD Market Update

11 Aug 2026 • 00:30 GMT

The Singapore dollar (SGD) remains relatively stable against major currencies, trading at around 0.7810 versus the US dollar. This level is just above its three-month average, with the pair trading within a narrow 2% range. Despite signs of US dollar strength due to market expectations of Federal Reserve tightening and rising energy prices, SGD shows resilience.

Looking ahead, market focus will be on potential monetary policy moves by Singapore’s Monetary Authority and upcoming US inflation data. If the US dollar continues to strengthen, the SGD could face some downside pressure, especially toward resistance levels near 0.7862. Conversely, if US inflation moderates as expected, the SGD might maintain its current range.

Against other currencies, the SGD has also shown stability near its averages, including against the euro and Australian dollar. Notably, the SGD has recently dipped to 7-day lows versus the British pound but remains within its typical trading range. Overall, the SGD continues to exhibit moderate movement, with external economic cues likely to determine if it gains or loses momentum in the coming weeks.

Forecast snapshot

Quick SGD/USD forecast

Near-term bias🔴 Mild downside

Expected range0.7760 – 0.7890

Dominant driver🌍 Global risk sentiment

3-month trend🔴 Downtrend

Stay informed

SGD news & insights

Recent analysis, guides and market developments relevant to the Singapore dollar.

Rate direction

Singapore dollar to US dollar · SGD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on SGD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore SGD pairs

Popular SGD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 SGD =0.7807USD

1D−0.2%▼

1 SGD =1.1073AUD

1D0.0%⬦

1 SGD =3.1939MYR

1D−0.2%▼

1 SGD =74.50INR

1D+0.1%▲

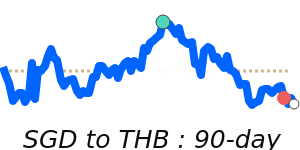

1 SGD =25.88THB

1D+0.1%▲

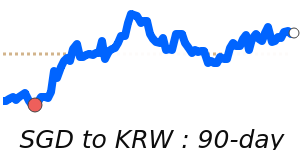

1 SGD =1,106.3KRW

1D+0.5%▲

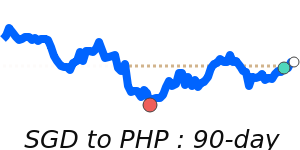

1 SGD =47.79PHP

1D0.0%⬦

1 SGD =6.1257HKD

1D−0.2%▼