Latest market analysis

ZAR Market Update

11 Aug 2026 • 00:32 GMT

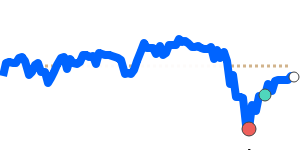

The South African rand has seen some notable movements against the US dollar recently. It is now trading below R16 per USD for the first time since mid-2022, reflecting a stronger rand overall. This rise is supported by a weaker US dollar, which has been pushed higher by expectations of Federal Reserve rate hikes and a decline in risk appetite for tech stocks. The USD's support is also fueled by higher energy prices and global geopolitical tensions, keeping the US dollar broadly firm.

The rand's current strength is also helped by positive signs in South Africa's economy, including improved electricity supply and better logistics, along with a new inflation target of 3%. Traders are also betting on further interest rate cuts in South Africa this year, which should support growth and keep the rand attractive.

While the rand remains relatively stable overall, ongoing geopolitical developments and US monetary policy changes could influence its future direction. For now, the rand's recent move below R16/$ marks a positive shift for the local currency. Keep an eye on global risks and South African economic data that might impact this trend.

Forecast snapshot

Quick ZAR/USD forecast

Near-term bias🔴 Mild downside

Expected range0.0610 – 0.0620

Dominant driver🌍 Global risk sentiment

3-month trend🔴 Downtrend

Stay informed

ZAR news & insights

Recent analysis, guides and market developments relevant to the South African rand.

Rate direction

US dollar to South African rand · USD/ZAR trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on ZAR exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore ZAR pairs

Popular ZAR exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 ZAR =0.061564USD

1D−0.2%▼

1 ZAR =0.053369EUR

1D−0.1%▼

1 ZAR =0.085815CAD

1D−0.3%▼

1 ZAR =0.045605GBP

1D−0.3%▼

1 ZAR =5.8748INR

1D0.0%⬦

1 ZAR =9.8079JPY

1D+0.7%▲

1 ZAR =0.087301AUD

1D−0.1%▼

1 ZAR =0.078872SGD

1D0.0%⬦

1 ZAR =0.4154CNY

1D−0.2%▼