Latest market analysis

CAD Market Update

31 Jul 2026 • 00:27 GMT

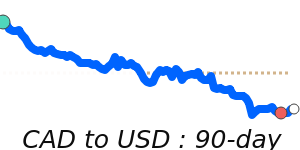

The Canadian dollar is trading near 30-day highs against the US dollar at around 0.7138, just below its three-month average. The recent stability in the USD/CAD exchange rate reflects a balanced market, with the loonie holding within a comfortable range from 0.7026 to 0.7358 over the past month.

However, the Canadian dollar has faced some pressure this week due to declining oil prices, which are now around US$79.40. As oil is a key export for Canada, lower prices can weigh on the CAD’s strength, especially if oil continues to slide. Additionally, ongoing global uncertainties and concerns about US economic outlooks add to the cautious tone.

Looking ahead, many analysts remain divided on where USD/CAD is headed by year-end, with forecasts ranging from 1.34 to 1.40. For now, the loonie’s position appears comfortably supported near current levels, but traders should keep an eye on oil prices and US economic indicators that could influence the pair’s next move.

Forecast snapshot

Quick CAD/USD forecast

Near-term bias🔴 Mild downside

Expected range0.7230 – 1.3400

Dominant driver🌍 Global risk sentiment

3-month trend⚪ Range-bound

Stay informed

CAD news & insights

Recent analysis, guides and market developments relevant to the Canadian dollar.

Rate direction

Canadian dollar to US dollar · CAD/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on CAD exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore CAD pairs

Popular CAD exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 CAD =0.7130USD

1D+0.3%▲

1 CAD =0.6203EUR

1D−0.2%▼

1 CAD =12.37MXN

1D−0.3%▼

1 USD =0.8701EUR

1D−0.5%▼

1 CAD =68.03INR

1D+0.2%▲

1 CAD =0.5307GBP

1D−0.4%▼

1 CAD =43.68PHP

1D+0.1%▲

1 CAD =1.0148AUD

1D−0.7%▼

1 INR =0.014700CAD

1D−0.2%▼