Latest market analysis

MYR Market Update

10 Aug 2026 • 00:33 GMT

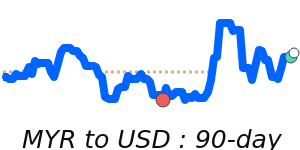

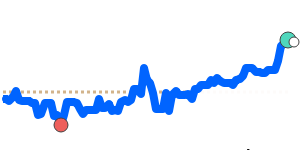

The Malaysian Ringgit remains relatively steady against the US dollar, trading at around 0.2445. This level is just slightly below its three-month average of 0.2468, indicating a stable period with limited volatility. The MYR has generally traded within a narrow range of 5.8%, between roughly 0.2410 and 0.2549, reflecting balanced factors supporting its strength.

Support for the ringgit continues to come from Malaysia's resilient economy and positive foreign investment flows, as highlighted by recent forecasts. Experts, including MUFG and UOB, project the MYR to appreciate gradually, with projections around the 3.85 to 3.90 range versus the dollar by year-end, and some forecasts suggesting a potential move toward 3.70.

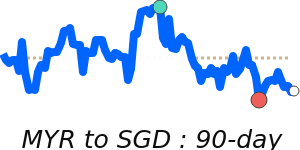

In comparison, the MYR has softened slightly against other major currencies like the euro, GBP, and JPY, where the pulls are modest but noticeable. against the yen, the MYR is at 38.60, around 2.5% below its three-month average, indicating a slight weakening in that pairing.

Overall, the ringgit’s outlook remains cautiously optimistic, supported by Malaysia’s economic fundamentals and external factors. No significant shifts are expected unless there are unforeseen changes in global energy prices or US monetary policy.

Forecast snapshot

Quick MYR/USD forecast

Near-term bias🔴 Mild downside

Expected range0.2450 – 0.2550

Dominant driver🌍 Global risk sentiment

3-month trend🟢 Uptrend

Stay informed

MYR news & insights

Recent analysis, guides and market developments relevant to the Malaysian ringgit.

Rate direction

US dollar to Malaysian ringgit · USD/MYR trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on MYR exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore MYR pairs

Popular MYR exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 MYR =0.2446USD

1D0.0%⬦

1 MYR =0.3129SGD

1D0.0%⬦

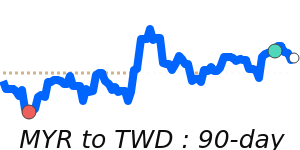

1 MYR =7.8772TWD

1D0.0%⬦

1 MYR =0.3465AUD

1D0.0%⬦

1 MYR =1.9187HKD

1D0.0%⬦

1 MYR =23.29INR

1D+0.1%▲

1 MYR =1.6500CNY

1D0.0%⬦

1 MYR =14.86PHP

1D+0.2%▲