Latest market analysis

AED Market Update

04 Aug 2026 • 00:35 GMT

The UAE Dirham (AED) remains steady against the US dollar, maintaining its 3-month average of 0.2723. This stability reflects ongoing confidence in the UAE's economic outlook amid recent developments. The introduction of the Digital Dirham signals modernization efforts, and although it has not yet caused noticeable currency shifts, it underscores the country's push for digital financial infrastructure.

Meanwhile, the USD continues to show strength overall, supported by global energy prices and geopolitical factors. Despite some fluctuations in other currencies, the AED’s rate against USD remains notable for its stability. Against major currencies like the euro and pound, the AED also remains stable, trading very close to its recent averages.

Overall, there is no significant movement in the AED, and it continues to trade within a narrow range, backed by positive economic policies and infrastructure projects. Market participants can expect the AED to stay relatively steady in the near term, pending any major geopolitical or economic shifts.

Stay informed

AED news & insights

Recent analysis, guides and market developments relevant to the United Arab Emirates dirham.

Rate direction

US dollar to United Arab Emirates dirham · USD/AED trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on AED exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore AED pairs

Popular AED exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 AED =0.2723USD

1D0.0%⬦

1 AED =25.89INR

1D0.0%⬦

1 AED =0.2024GBP

1D+0.5%▲

1 AED =75.61PKR

1D+0.3%▲

1 AED =0.3491SGD

1D+0.1%▲

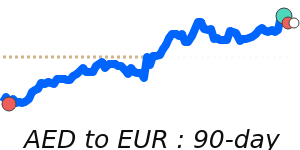

1 AED =0.2361EUR

1D+0.3%▲

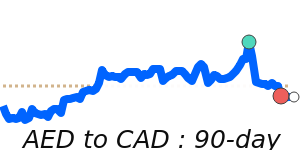

1 AED =0.3830CAD

1D+0.3%▲

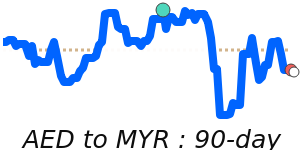

1 AED =1.1156MYR

1D+0.3%▲

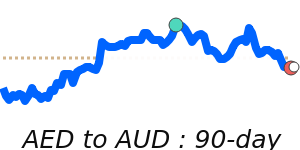

1 AED =0.3863AUD

1D+0.7%▲