Latest market analysis

GBP Market Update

08 Aug 2026 • 01:24 GMT

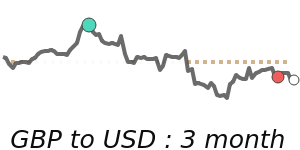

The British Pound has been climbing, reaching a 14-day high near 1.3493 against the US dollar. This marks a slight uptick of less than 1% above its recent 3-month average of around 1.3388 and reflects a period of relative stability, with the pair trading within a narrow range. The overall trading has been quite steady, with fluctuations staying within a 3.5% band from 1.3168 to 1.3634.

Market participants remain attentive to UK political developments and the Bank of England's policy stance. Despite ongoing leadership concerns, the BoE’s hints of potential rate hikes continue to support the pound, especially amid rising UK gilt yields. Meanwhile, the broader dollar remains resilient amid global energy tensions and geopolitical risks, which continue to influence currency movements.

While forecasts vary—some expecting GBPUSD to edge as high as 1.39 later this year—the current sentiment suggests cautious optimism. For now, the pound's stability against the dollar highlights a market balancing political uncertainties with signals of monetary tightening. Keep an eye on political news and upcoming UK economic data, as these could shift the pound's trajectory.

Forecast snapshot

Quick GBP/USD forecast

Near-term bias🟢 Mild upside

Expected range1.3490 – 1.3870

Dominant driver🌍 Global risk sentiment

3-month trend🟢 Uptrend

Stay informed

GBP news & insights

Recent analysis, guides and market developments relevant to the British pound.

Rate direction

British pound to US dollar · GBP/USD trend

Review the recent market direction, current mid-market rate and significant movement alerts.

Compare before you exchange

Compare and save on GBP exchange rates

Exchange rates vary between banks and currency providers. Use the comparison below to understand total costs and potential savings against typical bank pricing.

Loading exchange rates...

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

Explore GBP pairs

Popular GBP exchange rates

Open a currency pair to view its live rate, comparison options, recent trend and market context.

1 GBP =1.3491USD

1D+0.3%▲

1 GBP =1.1669EUR

1D0.0%⬦

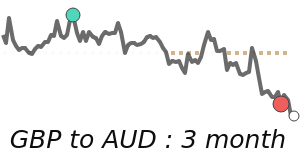

1 GBP =1.9093AUD

1D−0.2%▼

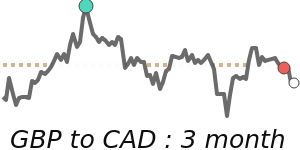

1 GBP =1.8821CAD

1D−0.2%▼

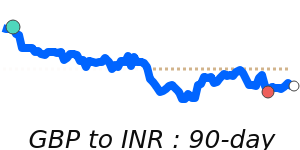

1 GBP =128.35INR

1D+0.2%▲

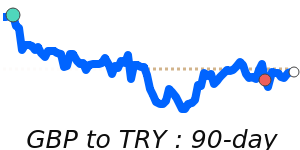

1 GBP =64.35TRY

1D+0.4%▲

90dHighs

1 GBP =4.9552AED

1D+0.3%▲

1 GBP =2.2889NZD

1D−0.1%▼

1 GBP =5.5180MYR

1D+0.2%▲

1 GBP =21.78ZAR

1D−1.0%▼