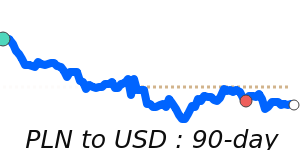

PLN Market Update

18 Jul 2026 • 01:13 GMT

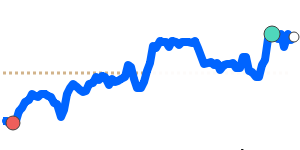

The Polish zloty (PLN) remains somewhat subdued against the US dollar, trading at around 0.2636, which is about 2.9% below its recent three-month average of 0.2716. The currency has stayed within a stable range, between approximately 0.2627 and 0.2786, despite the dollar’s overall support from rising energy prices and geopolitical tensions in the Middle East.

The dollar is still benefiting from higher energy costs and geopolitical developments, which tend to boost the currency during uncertain times. While the zloty has shown some weakness compared to the dollar, its declines are in line with recent stable trading patterns.

Poland's solid economic growth prospects and lower inflation rate provide some support for the zloty in the longer term. However, current market sentiment remains cautious, especially with external factors such as oil prices influencing the USD. For now, the zloty continues to trade in a narrow range, reflecting a market that is watching global energy prices and geopolitical developments closely.

📊 Quick forecast view

🔴 Mild downside

0.2580 – 0.2640

🌍 Global risk sentiment

⚪ Range-bound